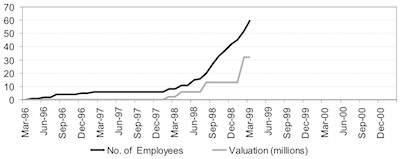

Neoforma, Inc., the online leader in the business-to-business global electronic healthcare marketplace, today announced it has completed a $12 million third round of equity funding led by Delphi Ventures. The round also included investments by TCW/ICICI Investment Partners, Venrock Associates, Amerindo Investment Advisors, MedVenture Associates, TTC Ventures, and Comdisco Ventures.

Neoforma Press Release, March 9, 1999

I was feeling much better about things. Experience should have warned me that this was a bad sign.

The website had steadily improved over the previous couple of months. I still wasn’t happy with it as a whole, but I was very happy with parts of it...

The website had steadily improved over the previous couple of months. I still wasn’t happy with it as a whole, but I was very happy with parts of it...

I focused most of my time on the capital equipment planning portion of the website. I was glad to have the luxury of having my hands on the product again. I was helping to create something and I was able to attend trade shows and meet with the customers who were benefiting from our work.

I was getting better at releasing things, without letting go, and at subtly guiding others, without infringing upon their need to control their own outcomes. I was getting better at accepting the choices of others, even when I disagreed with them. I was learning that I could trust others to get it right—if not the first time, then at least by the second or third.

In other words, I was backing off, giving everyone else—and myself—a break. My drive to do more and better, right now, was dissipating into a desire to do more and better, eventually. My newly relaxed work style provided me with a better perspective on what a pain-in-the-butt I could be.

And now, only the capital planning group had to deal with my fussy side. But even there, I had delegated much of my authority to someone I trusted. So I would only irritate people here and there, now and then.

I was becoming an active observer rather than a central force and the break was nice. It gave me the opportunity to release some of the last three years’ stress.

When I’d stare out of my office window at the cubicles beyond, I’d notice an argument or bit of celebratory distraction and enjoy the momentary equilibrium between my need to interfere and my need to let it go. I wasn’t disengaged. I was simply more balanced.

Neoforma was back in the fundraising mode. I wasn’t much involved in it. Alexander and JP were setting up meetings with name-brand VCs. Jeff was attending them. Well, actually, he was doing more than just attending them. Since the close of our first venture round and this upcoming second one, Jeff had educated himself in the nature of the venture capital world. He was paying attention to the details and motivations that had been irrelevant in our money-starved days.

As I stepped back from power, Jeff stepped forward. He was certainly charismatic and intelligent enough to lead, but he wasn’t enjoying himself. He liked the challenge, but he had less patience for unmotivated or dependent personalities than I did.

As he became increasingly embroiled in the world of venture capitalists, Jeff began to express to me his concerns about the true motivations of some of our investors.

Even though I only attended a few of the key VC meetings, Jeff and I spoke nearly every day, discussing the various pros and cons of each option Neoforma faced. Jeff knew that his vote alone was not enough to direct any decision. He had to convince me to look out for myself too. He became increasingly angry when I wouldn’t accept the idea that there were some who would, without a thought, screw us for personal gain.

Jeff had become convinced that a possible objective of the outside investors was to separate the founders—Jeff and me—and earliest angel investors, from of our share of the company in order to increase their returns. As our next funding round approached, Jeff became more concerned about protecting our investment in Neoforma. Rising to the occasion, he proceeded to learn the workings and language of venture capital with lightning speed and admirable proficiency.

Now that we were backed by a tier-one venture firm, blossoming press coverage and a stimulated financial market, we had many options to choose from.

Jeff learned that some of the investment terms favored outside investors rather than the founders. One distinguishing factor was the

valuation of the company. Jeff had been able to solicit a term sheet at an attractive valuation from one of the tier-one firms. He felt that the long-term benefit of strong, active partners was more important than a higher valuation. Bret and JP, in particular, insisted that we could get perfectly good money, at a higher valuation, from slightly less renowned VCs.

Jeff’s fears were confirmed when each of the term sheets arrived. These documents outlined the details of a deal. Mostly they covered who gets to keep what in the event of liquidation—either through the failure, sale or public offering of the company. Somehow, in the details of the high valuation deals, a clause dealing with participating preferred stock had been inserted. These provisions addressed what would happen in the event of the sale of the company before an IPO.

The term participating preferred meant that if the company were sold, the most recent investors would get their money first. Not only that, but they would be guaranteed a multiple of their original investments before any remaining money was distributed to earlier investors. So in some scenarios, the latest investors could get two or three times their money back, while early investors could potentially get nothing.

Foolishly, this idea didn’t bother me much at the time. After all, we were talking about large amounts of money. The investors deserved a fair chance at a good return. I didn’t like the idea of them getting three times their investment, but one-and-a-half or two times didn’t seem unreasonable. And when it came down to it, I refused to consider the possibility that the company would be sold for less than the amount that would yield Jeff and me a good return.

Jeff didn’t see things this way at all. How dare these investors think that their money was somehow worth more than our years of labor? This just confirmed his belief that, as soon as they owned more of the company than Jeff and I combined, these investors would be quite content to sell the company for a quick return to them, independent of the value to us or to the employees. Under the terms of these agreements, the company could be sold for $60 million or more and Jeff and I wouldn’t get a penny. Most of all, he wondered how these terms got in deals anyway. It turns out that their insertion had been suggested to the new VCs by our own friendly investors as a means to assure future them that their money was safe at a higher valuation. This was fine for them—they would be included in the preferred group. But Jeff and I and the early angels wouldn’t.

I thought we should be able to negotiate some kind of compromise. Jeff was furious at me for my naïveté and disloyalty.

To the chagrin of Bret, JP and Alexander, Jeff adamantly refused to accept these clauses. He was confident that he could secure an attrac- tive deal without the preferred clause. Bret and company did not want to wait.

Playing the role of a tough negotiator, he simply refused to work with the deals that favored our recent investors over our early investors.

About a week before the deciding Board meeting, while enjoying a moment of my newly balanced contemplation at my desk, I was suddenly interrupted by a fiery Greek storming into my office and firmly closing the door. Alexander was hyperventilating—pacing two steps forward and two steps back, two steps forward, two steps back. His arms were tense, his muscles quivering. He held his hands outstretched in front of him, palms up. It was as if he were lifting a heavy box—getting ready to throw it, then calming himself, lowering the box—then getting angry again, lifting it to throw it—and so on.

I waited while he tried to compose himself enough to tell me what was on his mind. He eventually managed to say, “WAYNE, WE’VE GOT TO TALK. JEFF IS DRIVING ME NUTS. HE IS POSITIVELY INSANE. HE’S GOING TO KEEP US FROM GETTING THIS FUNDING ROUND CLOSED. YOU HAVE TO BE PREPARED TO TAKE OVER. THE REST OF THE BOARD WANTS YOU TO TAKE OVER AT THE NEXT BOARD MEETING.”

By now, Jeff had become sufficiently hostile to me and everyone else that I was not particularly surprised by this request. But that didn’t make me any more comfortable with it. Since founding Neoforma, Jeff and I had disagreed on many issues, big and small. But we had always managed to compromise. And in spite of our differences, we had always displayed a unified face to the rest of the world.

Now I had been asked to not only disagree with him, but to throw him out of the company. Putting aside my feelings of loyalty for a moment, I couldn’t help but go along with Alexander’s point. Jeff had told me that he would quit before he would accept the proposed deals.

Everything we had built was suddenly at risk. Unless I was able to calm Jeff down, he was in danger of severely injuring the company.

As if awakened from a dream, I jumped out of my finely balanced retreat and surveyed the environment. I called some of the most recent investors. They too were frustrated by Jeff’s seemingly intractable position. They were telling me that my moderate voice was what the company needed right now. In the face of a one-sided advantage to a few, Jeff did not appear to be open to moderation. Of course, what they were really doing was massaging my ego and telling me that I was the only one who could legitimately take over without upsetting the potential new investors.

So I called a few of our early angel investors. I needed their advice and I felt a duty to inform them that Alexander, JP, led by Bret thought I might need to take over the company. Instead of jumping on the bandwagon with the others, they acknowledged the merits of Jeff’s argument.

As early investors, they would be only one level above Jeff and me from the bottom of the list if the company were sold. And they didn’t necessarily trust the motivations of the later investors either.

None of them liked the participating preferred clauses, but they had come to accept them as a necessary evil. They weren’t happy with the situation, but they were also afraid what Jeff might do and gave me their support should I get left holding the bag. They liked Jeff, but they had enough experience with him to fear his stubbornness. They had to protect their investments.

That’s how I felt too. I hated the idea of going against Jeff in favor of largely unknown future investors, but I couldn’t let him jeopardize the company. I put my deeper feelings on hold. I had a job to do.

On the day before I was to take the reins, I made a last-ditch effort to bring Jeff and Bret to a state of compromise. Bret indicated a little flexibility, but he was so upset with Jeff that he dismissed the idea of even considering a compromise.

For his part, Jeff was barely willing to speak with me. He was disgusted with me, convinced that I was being led to the slaughter by the vicious VCs. But I was able to discuss the issue with him. That was progress.

He unhappily said that at this point he was willing to consider a compromise position on the participating preferred clause. If we could get the new investors to accept a significantly smaller multiple in their preference—meaning they would only get a little bit more than us in the event of a sale of the company—then he might be able to accept it. He’d think about it, anyway, and let us know at the Board meeting tomorrow. I allowed myself a moment of hope.

Because of the number of legal issues that might need to be dealt with at a meeting—both about approving a funding round and changing a CEO—this Board meeting was held in a conference room at our attorney’s office.

It was a breezy, overcast morning. I walked into the building in a daze. I did not want to see any of the attendees before the meeting, so I arrived exactly on time. I silently nibbled on sweet rolls and sipped coffee, while the other attendees trickled into the room and greeted each other quietly. The somber mood in the room was not typical of a meeting about closing a twelve million dollar funding round.

I was the only one who had any hope that Jeff would still be in his job the next day. I knew that Jeff would often take extreme positions as a negotiating tactic, but I wasn’t sure what he’d do this time. Jeff was out of town and would only be calling in to the meeting. This would make it very difficult to read Jeff’s intent. Bret was also calling in from his vacation in Europe. Before Jeff got on the line, I told the Board that I thought Jeff might accept a suitable compromise position. They didn’t believe me.

When Jeff did get on the phone, he acted curt and indignant, but he did accept the compromise position for the sake of the company. Then he hung up.

It looked like I was off the hook for the time being. However, my short-lived peace of mind had been irrevocably jolted. I knew now that, even when things looked okay, I had to be ready for anything. Doing my job would never be enough.

Jeff and I didn’t speak much for many months. I had always thought of him as a business partner. No more. Now I felt the absence of a friend.

And as much as I had disagreed with the inflexibility of Jeff’s position on the funding round, I did agree with him on one thing—my new partners, the VCs, were certainly not my friends. I had allowed them to manipulate me into putting my fear of losing everything above my loyalty to a friend.

I was getting better at releasing things, without letting go, and at subtly guiding others, without infringing upon their need to control their own outcomes. I was getting better at accepting the choices of others, even when I disagreed with them. I was learning that I could trust others to get it right—if not the first time, then at least by the second or third.

In other words, I was backing off, giving everyone else—and myself—a break. My drive to do more and better, right now, was dissipating into a desire to do more and better, eventually. My newly relaxed work style provided me with a better perspective on what a pain-in-the-butt I could be.

And now, only the capital planning group had to deal with my fussy side. But even there, I had delegated much of my authority to someone I trusted. So I would only irritate people here and there, now and then.

I was becoming an active observer rather than a central force and the break was nice. It gave me the opportunity to release some of the last three years’ stress.

When I’d stare out of my office window at the cubicles beyond, I’d notice an argument or bit of celebratory distraction and enjoy the momentary equilibrium between my need to interfere and my need to let it go. I wasn’t disengaged. I was simply more balanced.

Neoforma was back in the fundraising mode. I wasn’t much involved in it. Alexander and JP were setting up meetings with name-brand VCs. Jeff was attending them. Well, actually, he was doing more than just attending them. Since the close of our first venture round and this upcoming second one, Jeff had educated himself in the nature of the venture capital world. He was paying attention to the details and motivations that had been irrelevant in our money-starved days.

As I stepped back from power, Jeff stepped forward. He was certainly charismatic and intelligent enough to lead, but he wasn’t enjoying himself. He liked the challenge, but he had less patience for unmotivated or dependent personalities than I did.

As he became increasingly embroiled in the world of venture capitalists, Jeff began to express to me his concerns about the true motivations of some of our investors.

Even though I only attended a few of the key VC meetings, Jeff and I spoke nearly every day, discussing the various pros and cons of each option Neoforma faced. Jeff knew that his vote alone was not enough to direct any decision. He had to convince me to look out for myself too. He became increasingly angry when I wouldn’t accept the idea that there were some who would, without a thought, screw us for personal gain.

Jeff had become convinced that a possible objective of the outside investors was to separate the founders—Jeff and me—and earliest angel investors, from of our share of the company in order to increase their returns. As our next funding round approached, Jeff became more concerned about protecting our investment in Neoforma. Rising to the occasion, he proceeded to learn the workings and language of venture capital with lightning speed and admirable proficiency.

Now that we were backed by a tier-one venture firm, blossoming press coverage and a stimulated financial market, we had many options to choose from.

Jeff learned that some of the investment terms favored outside investors rather than the founders. One distinguishing factor was the

valuation of the company. Jeff had been able to solicit a term sheet at an attractive valuation from one of the tier-one firms. He felt that the long-term benefit of strong, active partners was more important than a higher valuation. Bret and JP, in particular, insisted that we could get perfectly good money, at a higher valuation, from slightly less renowned VCs.

Jeff’s fears were confirmed when each of the term sheets arrived. These documents outlined the details of a deal. Mostly they covered who gets to keep what in the event of liquidation—either through the failure, sale or public offering of the company. Somehow, in the details of the high valuation deals, a clause dealing with participating preferred stock had been inserted. These provisions addressed what would happen in the event of the sale of the company before an IPO.

The term participating preferred meant that if the company were sold, the most recent investors would get their money first. Not only that, but they would be guaranteed a multiple of their original investments before any remaining money was distributed to earlier investors. So in some scenarios, the latest investors could get two or three times their money back, while early investors could potentially get nothing.

Foolishly, this idea didn’t bother me much at the time. After all, we were talking about large amounts of money. The investors deserved a fair chance at a good return. I didn’t like the idea of them getting three times their investment, but one-and-a-half or two times didn’t seem unreasonable. And when it came down to it, I refused to consider the possibility that the company would be sold for less than the amount that would yield Jeff and me a good return.

Jeff didn’t see things this way at all. How dare these investors think that their money was somehow worth more than our years of labor? This just confirmed his belief that, as soon as they owned more of the company than Jeff and I combined, these investors would be quite content to sell the company for a quick return to them, independent of the value to us or to the employees. Under the terms of these agreements, the company could be sold for $60 million or more and Jeff and I wouldn’t get a penny. Most of all, he wondered how these terms got in deals anyway. It turns out that their insertion had been suggested to the new VCs by our own friendly investors as a means to assure future them that their money was safe at a higher valuation. This was fine for them—they would be included in the preferred group. But Jeff and I and the early angels wouldn’t.

I thought we should be able to negotiate some kind of compromise. Jeff was furious at me for my naïveté and disloyalty.

To the chagrin of Bret, JP and Alexander, Jeff adamantly refused to accept these clauses. He was confident that he could secure an attrac- tive deal without the preferred clause. Bret and company did not want to wait.

Playing the role of a tough negotiator, he simply refused to work with the deals that favored our recent investors over our early investors.

About a week before the deciding Board meeting, while enjoying a moment of my newly balanced contemplation at my desk, I was suddenly interrupted by a fiery Greek storming into my office and firmly closing the door. Alexander was hyperventilating—pacing two steps forward and two steps back, two steps forward, two steps back. His arms were tense, his muscles quivering. He held his hands outstretched in front of him, palms up. It was as if he were lifting a heavy box—getting ready to throw it, then calming himself, lowering the box—then getting angry again, lifting it to throw it—and so on.

I waited while he tried to compose himself enough to tell me what was on his mind. He eventually managed to say, “WAYNE, WE’VE GOT TO TALK. JEFF IS DRIVING ME NUTS. HE IS POSITIVELY INSANE. HE’S GOING TO KEEP US FROM GETTING THIS FUNDING ROUND CLOSED. YOU HAVE TO BE PREPARED TO TAKE OVER. THE REST OF THE BOARD WANTS YOU TO TAKE OVER AT THE NEXT BOARD MEETING.”

By now, Jeff had become sufficiently hostile to me and everyone else that I was not particularly surprised by this request. But that didn’t make me any more comfortable with it. Since founding Neoforma, Jeff and I had disagreed on many issues, big and small. But we had always managed to compromise. And in spite of our differences, we had always displayed a unified face to the rest of the world.

Now I had been asked to not only disagree with him, but to throw him out of the company. Putting aside my feelings of loyalty for a moment, I couldn’t help but go along with Alexander’s point. Jeff had told me that he would quit before he would accept the proposed deals.

Everything we had built was suddenly at risk. Unless I was able to calm Jeff down, he was in danger of severely injuring the company.

As if awakened from a dream, I jumped out of my finely balanced retreat and surveyed the environment. I called some of the most recent investors. They too were frustrated by Jeff’s seemingly intractable position. They were telling me that my moderate voice was what the company needed right now. In the face of a one-sided advantage to a few, Jeff did not appear to be open to moderation. Of course, what they were really doing was massaging my ego and telling me that I was the only one who could legitimately take over without upsetting the potential new investors.

So I called a few of our early angel investors. I needed their advice and I felt a duty to inform them that Alexander, JP, led by Bret thought I might need to take over the company. Instead of jumping on the bandwagon with the others, they acknowledged the merits of Jeff’s argument.

As early investors, they would be only one level above Jeff and me from the bottom of the list if the company were sold. And they didn’t necessarily trust the motivations of the later investors either.

None of them liked the participating preferred clauses, but they had come to accept them as a necessary evil. They weren’t happy with the situation, but they were also afraid what Jeff might do and gave me their support should I get left holding the bag. They liked Jeff, but they had enough experience with him to fear his stubbornness. They had to protect their investments.

That’s how I felt too. I hated the idea of going against Jeff in favor of largely unknown future investors, but I couldn’t let him jeopardize the company. I put my deeper feelings on hold. I had a job to do.

On the day before I was to take the reins, I made a last-ditch effort to bring Jeff and Bret to a state of compromise. Bret indicated a little flexibility, but he was so upset with Jeff that he dismissed the idea of even considering a compromise.

For his part, Jeff was barely willing to speak with me. He was disgusted with me, convinced that I was being led to the slaughter by the vicious VCs. But I was able to discuss the issue with him. That was progress.

He unhappily said that at this point he was willing to consider a compromise position on the participating preferred clause. If we could get the new investors to accept a significantly smaller multiple in their preference—meaning they would only get a little bit more than us in the event of a sale of the company—then he might be able to accept it. He’d think about it, anyway, and let us know at the Board meeting tomorrow. I allowed myself a moment of hope.

Because of the number of legal issues that might need to be dealt with at a meeting—both about approving a funding round and changing a CEO—this Board meeting was held in a conference room at our attorney’s office.

It was a breezy, overcast morning. I walked into the building in a daze. I did not want to see any of the attendees before the meeting, so I arrived exactly on time. I silently nibbled on sweet rolls and sipped coffee, while the other attendees trickled into the room and greeted each other quietly. The somber mood in the room was not typical of a meeting about closing a twelve million dollar funding round.

I was the only one who had any hope that Jeff would still be in his job the next day. I knew that Jeff would often take extreme positions as a negotiating tactic, but I wasn’t sure what he’d do this time. Jeff was out of town and would only be calling in to the meeting. This would make it very difficult to read Jeff’s intent. Bret was also calling in from his vacation in Europe. Before Jeff got on the line, I told the Board that I thought Jeff might accept a suitable compromise position. They didn’t believe me.

When Jeff did get on the phone, he acted curt and indignant, but he did accept the compromise position for the sake of the company. Then he hung up.

It looked like I was off the hook for the time being. However, my short-lived peace of mind had been irrevocably jolted. I knew now that, even when things looked okay, I had to be ready for anything. Doing my job would never be enough.

Jeff and I didn’t speak much for many months. I had always thought of him as a business partner. No more. Now I felt the absence of a friend.

And as much as I had disagreed with the inflexibility of Jeff’s position on the funding round, I did agree with him on one thing—my new partners, the VCs, were certainly not my friends. I had allowed them to manipulate me into putting my fear of losing everything above my loyalty to a friend.

RSS Feed

RSS Feed