Burning Up: Warning: Internet Companies Are Running Out of Cash—Fast

When will the Internet Bubble burst? For scores of Net upstarts, that unpleasant popping sound is likely to be heard before the end of this year. Starved for cash, many of these companies will try to raise fresh funds by issuing more stock or bonds. But a lot of them won’t succeed. As a result, they will be forced to sell out to stronger rivals or go out of business altogether . . .

Barron’s, March 20, 2000

Neoforma.com Chief Bridges Old and New Economies

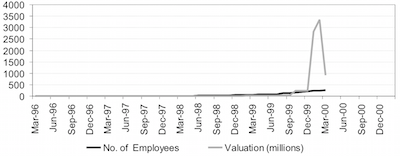

Robert Zollars is not your stereotypical Silicon Valley chief executive. Before taking over the top three posts at Neoforma.com . . . he spent nearly 20 years working his way up the corporate ladder of the healthcare products industry . . . After less than a year at the helm of Neoforma.com, he took the company public. It now boasts a hefty $3.3 billion market capitalization . . .

Forbes Magazine, March 28, 2000

Neoforma.com to Acquire Eclipsys

Neoforma.com Inc., operator of an online medical marketplace, agreed to acquire Eclipsys Corp., a healthcare software and services provider, and a related company for stock totaling $2.72 billion.

Associated Press, March 30, 2000

Over dinner one evening, I glanced up from my plate, assumed an air of casualness, and said to Anni, “We made twenty million dollars today.”

I just had to say it, once...

I just had to say it, once...

Anni frowned at me, scolding, “It’s not real, you know. It’s only on paper. Anything could happen.” I knew it was only paper, but even a fraction of that paper would get us out of debt. Anni would finally be able to quit the graphics job she dreaded more each day. She could finally catch up on a hundred unfinished projects. She could finally get back to fine art. I felt good about that.

But Anni had been well trained by her father, whose family had lived during the Depression . . . Nothing is real until it is real. I begged to differ. Nothing is real until someone imagines it to be real.

I did not want to act on an uncertain future, but neither did I want to deny it. While I have never been one to lean toward extravagance, I couldn’t help having some small fantasies about what I could do with some of this unexpected money.

I imagined creating and funding a guild of talented architects and craftspeople, dedicated to building the beautiful and experimental buildings I had visualized in my design school days. My new business skills could be creatively applied to a profession that I believed was sorely lacking in innovation. I just had to figure out a way to do it without becoming obsessed with or consumed by it.

This seemingly small rift between Anni’s caution and my optimism amplified all the other rifts that had developed over the past decade. I was trying to allow myself some hope that all of the sacrifices we had made would finally be, somehow, justified. She had seen enough hopes suffocated by my pursuit of this venture to be less optimistic.

Neoforma had been working for almost a year to come up with a way to work with Novation, the largest group purchasing organization, the big daddy of GPOs. Their mission was to save hospitals huge amounts of money by aggregating their spending, thereby getting a negotiating edge on the manufacturers.

On the other hand, the manufacturer’s job was to carve out for themselves as much of the healthcare bill as possible. To stay alive, the GPOs needed to carve out a significant part of the savings for themselves too. We walked into one big angry community of sharing with the naïve idea of saving everyone time and money by making the process more efficient.

Of the GPOs, Novation was not only the largest by a hair, but it had a reputation of being one of the most ethical—or maybe just the least belligerent. That kind of fit with Neoforma’s personality. If we could work out a deal with two thousand hospitals at once, our need to waste resources fighting inertia, one hospital at a time, would be nearly eliminated. Our ability to focus would be luxurious.

It was a simple matter of economics. Why should we have a large sales force to sell our services a couple of hospitals at a time, when Novation has already done that job? And why should Novation create an entire technology organization to improve their communication between their suppliers and their member hospitals when technology was not their business?

The GPOs had taken different approaches to fight the broad category they labeled “the dotcoms.” The second largest GPO had decided to aggressively build its own dotcom, investing $50 million to fight us. The third largest GPO had partnered with our second largest competitor, Ventro, which had been a company like us in the laboratory supply space.

Ventro, funded by Kleiner Perkins (KP), had come up with the ultimate way to turn their substantial equity value into astronomical equity value. Their idea was to take a successful public niche company, like one serving the laboratory market, and clone it to serve another niche, like healthcare. The plan was to spin out each company as a new public offering, and so on.

So they reached out and acquired a small, niche medical Internet supply-chain company, Promedix, for $20 million, and became our competitor overnight. At their request, we had spoken with Ventro several times in the past about partnership opportunities. But we were told by their representatives that their investors didn’t like the idea of sharing a large industry that they believed they could dominate. And then there was the ego of their CEO and co-founder, David Perry.

Mr. Perry had painted quite a picture of himself in the media. Thanks to the KP machine, his had been the first B2B supply-chain company to go public. And the company stock had done very, very well. Mr. Perry had taken the bulk of the public credit, becoming something of a rags-to-riches darling in the business press.

Ventro wasn’t satisfied with owning only one company in competion with Neoforma. Our position in the market was too strong. So they orchestrated a major play in the medical supply-chain space. They partnered with the third largest GPO, Broadlane, to create another business chasing Neoforma. With KP’s substantial interest in Medibuy and Ventro, they controlled our three largest competitors.

Novation made their decision in early 1999. They were going to partner with someone, rather than build their own marketplace. They had evaluated more than one hundred candidates for that partnership, but in the end, we like to think it was a cultural issue that swayed their final decision.

Neoforma’s culture, for better and worse, was driven by a standard of cooperation rather than of confrontation. This was ironic, because we had always been seen by the industry players as “an upstart interloper in a system that was already balanced quite well, thank you.”

Novation was a company with a culture similar in many ways to Neoforma, though different in one key way—they moved very, very slowly, by the standards of Neoforma.

It was clear from our first meetings in early 1999 that our com- panies were a good fit for each other. We shared common goals, from a cultural standpoint.

But they needed time—to think about the implications and objectives of a partnership, to discuss it with all of their key members, then make a decision based on the overwhelming consensus of hundreds of hospitals, then send that decision back around for review and consensus.

After all, this is how they made all of their decisions. Making those decisions, carefully and deliberately, was what Novation was all about. Their service was literally about making the decisions on which products to use for a large group of healthcare providers who use those products to save lives every day.

Their decision process dragged on and on. We had meeting after meeting, followed by weeks or months of silence, followed by more meetings. They were in no hurry. They knew that most new healthcare products or services took a decade or so to get into practice.

We weren’t on that kind of schedule. When we became a public company, many analysts had pointed out how beneficial, even critical, it was for Neoforma to partner closely with one or more GPOs. Lever- aging their power was central to maintaining our first mover status.

Novation wasn’t particularly impressed with our IPO success.

They kept saying they were close to making a final decision and they indicated that we were on the short list to be the beneficiary of that decision. But nothing really changed, except our market cap . . .

Which wasn’t really nothing anymore.

Although there had been no public disclosures, we had heard the gossip rampant throughout the healthcare industry that we were close to a deal to partner with Novation, and that Medibuy (or, The Bug, as we called them) was close to a deal to partner with Novation’s primary competitor, Premier, the second largest GPO.

The Bug was still struggling to pull together their IPO. We had been working with Novation in the background for so long that we had taken this pretty much for granted. When Novation continued to drag its feet after our IPO, Bob stepped up as CEO and kicked things into high gear. While Novation was far and away our first choice, due to its great cultural fit and dominant size, we couldn’t afford to just sit back and wait for something to happen.

In February, Bob boldly called the head of Premier and offered $1 billion for Premier’s electronic commerce business. Even for a business that managed about $30 billion worth of spending each year for its members, this was a hard number to ignore.

In contrast to Novation’s reputation as a company driven by process and consensus, Premier had a reputation for forcefulness. Bob, who understood every fiber of this industry, was betting that a decision by Premier would drive the other GPOs into action. This would quickly drive Premier to either us or The Bug.

His gamble was that, if Premier went to The Bug, Novation would accelerate their move to us. Either we would acquire a large number of Premier’s hospital customers or we would weaken KP’s hold on The Bug by substantially increasing Premier’s equity expectations.

Bob’s initiative did instigate a series of hastily assembled meetings between Premier and Neoforma. Premier seemed to take our offer very seriously. While the cultural match between the two companies was far from strong, our common drive toward quick decision was a welcome relief. A deal structure was quickly sent to the lawyers. It looked like Bob’s ploy had worked.

When we thought the deal had been all but formally signed, our execs investigated the housing availability in La Jolla, California, where Premier was headquartered. In addition to beaches and great weather, housing was available for a fraction of the astronomical Bay Area housing costs. They liked that.

Then we heard some disturbing rumors from friends in the industry. Premier’s negotiations with us were a guise.

Premier figured they could trump The Bug by saying that if they didn’t receive a much larger piece of Medibuy than they were going to get from Neoforma, they were going to do a deal with Neoforma. That would practically squash The Bug’s hopes of going public.

And until The Bug caved in, Premier could keep Neoforma from proceeding with Novation, by pretending that they were still proceeding with us as planned. That way, they could announce the merger with The Bug as part of an IPO filing, garnering maximum buzz. Premier and The Bug were convinced that their public valuation would far exceed ours because of the aggressive nature of their mutual businesses.

Hey, it was business. Nasty stuff, but you had to play tough to get on top.

Once we validated these rumors, only a week before the deal was to be publicly announced, we feigned ignorance of the Medibuy deal, calmly stalled all dialog with Premier and notified Novation that we had heard that Premier was going to announce a deal with Medibuy very soon.

Novation may have been the quiet force among these fiercely competitive GPOs, but they were the largest. And their lead against number-two Premier was not very great. They knew a threat when they saw one.

By the time the hastily assembled Premier/Medibuy deal was announced in early March, Novation was wide awake. They were intensifying their talks with us. The preferred outcome to Bob’s plan was working out as planned. However, Novation, in negotiating the best possible deal they could, had made it clear that we had only made it to the short list. We had not yet been selected as the finalist.

As the press speculated about who Neoforma and Novation would partner with, we couldn’t help but look at our future without Novation. If Medibuy were to go public with a huge GPO partner and we did not partner with the only other one that mattered, we could be propelled from the clear market leader to a bit player, overnight.

The tension at Neoforma was very high. We all tried to pursue our assorted tasks with typical enthusiasm, but we knew that our fate was about to change dramatically, one way or the other.

Most of the time though, we assumed that an agreement with Novation was inevitable. That is, until our stock value began to decline. While our stock had climbed as high as $78, it had seemed to settle in the low fifties in early March. However, speculation about how critical a Novation deal was to Neoforma, combined with assorted jitters in the press about how new companies could suffer if the economy slowed down, began to nibble, day by day, at our stock value. By mid-March, our stock had drifted down into the thirties.

Bob had always made sure to emphasize that, as a newly public company, our stock price would be volatile. So we should not be concerned if it went down. We had a lot of work to do before our company grew to fill our market cap.

During our IPO party, Bob did allow a rare moment of indulgence, when he announced: “As of last week, Neoforma now has over a hundred millionaires!” Needless to say, those hundred millionaires cheered heartily at this boast.

Bob didn’t express concern to me about the stock price decline until it dropped into the twenties in late March—the week before our deal with Novation was due to be announced.

“It’s easy to give away a large, but minority, piece of Neoforma to get a deal for a third of the U.S. healthcare market, when our stock is in the fifties or even the forties,” Bob told me. “When it’s in the thirties, our negotiating position becomes much weaker. And in the twenties, it’s nearly impossible.”

For the first and only time, I saw panic in his eyes. For a moment, his innate certainty that his abilities could get him through anything seemed to be faltering. He saw the possibility that we might lose the deal and did not like it.

Once Novation decided to move forward with an Internet initiative, they decided that the best way to ensure quick adoption by hospitals was to incentivize the hospitals that signed up early. The best incentive for the nation’s struggling hospitals was money. And the best way to get that money to the hospitals would be to distribute Neoforma stock to them.

One of Novation’s key missions was to increase the quality of products purchased while saving money for their hospital members. Any money Novation made beyond what was required to support them went back to their members. The only way for all members to fully benefit from an automated commerce system would be to ensure wide adoption of a single solution. Returning money to their membership hospitals was consistent with their way of doing business.

The only problem was that, once they had set their expectation of how much money that would be, it would be hard to adjust to an increasingly lower number.

But the bigger problem was that Novation and their owners felt the need to combine their other software partnerships into one big new solution. They were insistent about it.

Novation had partnered extensively with a healthcare information technology firm called Eclipsys. They had even created a joint venture, HEALTHvision, targeted at helping hospitals set up their own websites. Novation wanted to trump the Medibuy/Premier deal by uniting these companies together into a single initiative. They wanted to add one plus one plus one to make ten.

This arrangement was not popular at Neoforma, to say the least.

First of all, Eclipsys was a large legacy. In other words, it was a maker of cumbersome, difficult-to-update software with well over a thousand employees. They were far from the largest player in health- care information technology (IT), but far from the smallest too.

Most of the software they developed wasn’t Internet software. And its applications served needs across the entire hospital, not just the supply-chain.

But Novation insisted that any solution they embraced needed to accommodate a transition from their older IT initiatives to their new ones. Novation wanted to include them in the deal—or else there would be no deal at all.

I had an aesthetic aversion to the idea of diluting the purity of our Internet model with an older technology solution. On the other hand, I had been in the healthcare market long enough to recognize that the newest solution is not always the one that will be adopted by this sluggish industry. But I knew this would be a pretty gutsy move, putting us in competition with some of the largest IT companies serving healthcare. And that might be fun.

Eclipsys had the challenge of moving from a legacy software provider into an Internet solution provider. Neoforma had the challenge of nudging the Industry’s inertia in our direction. It just might work.

Then I received a call from Debbie, an associate of one of our investors, who had heard that we might be partnering with Eclipsys. Her usually cheerful voice edged with panic, she said, “There’s someone you must speak with before you let this happen!” She asked if we could get together on the East Coast next week.

Jeff and I had a customer visit to New York already scheduled. We agreed to meet her mysterious person there.

When Jeff and I arrived at the trendy New York restaurant, Debbie and Dale were already seated at an appropriately private table. Dale was a friendly man, a decade or two our senior. He seemed like a man who had seen just about everything. He was a senior executive at one of the largest healthcare IT companies and had worked closely with the CEO of Eclipsys many times over the last several decades.

Dale spun a yarn about a man who was simultaneously despised, feared and respected throughout the healthcare industry; a man known—among his employees as well as his competitors—for his viciousness; a man appreciated on Wall Street for his singular focus on the stock value.

“This man will take Neoforma, strip it, and sell it for parts,” Dale said, with conviction. “He lives on the edge. His current company is

struggling with its old, underperforming software. He has been having greater difficulty each quarter meeting his numbers. He is just looking for some fresh meat to chew. And believe me, he’s done this many times before. He is a fierce survivor.”

My heart sunk as I listened to this summary of the man who would become the number-two guy at Neoforma. What would this do to the culture I had so carefully constructed? How could I let this happen?

On the other hand, the way the stock had been sinking, maybe we needed an experienced survivor on our team. Neoforma was going to be the acquirer. Maybe the Neoforma culture was strong enough to survive the influx of an extra thousand or so people. Ultimately, we had little choice in the matter. Our new knowledge would only make my suffering that much more exquisite.

After weeks of intense negotiation, from which I was completely isolated, the day for the public announcement was finally selected.

The press and analysts expressed increasing concern over our lack of a GPO partner. Our stock continued its slide into the low twenties. But we knew that the stock would soar again on the news that we had partnered with the huge GPO. How else could investors react to the announcement of two thousand new hospital customers?

The announcement was scheduled for a Tuesday. The release was being carefully orchestrated. Neoforma, Eclipsys and Novation execs were going to carefully present the new company to key investors, analysts and press contacts. Each company would enthusiastically present a unified vision to its employees.

Then, on the Tuesday a week before the big day, Jeff received a call from a reporter he had spoken with in the past. “I’m doing a story tomorrow on your upcoming merger with Eclipsys,” the reporter said. “I was wondering if you’d like to comment?” He disclosed enough details on the deal structure to verify that someone had leaked every detail of the merger.

In addition to being very angry that someone had leaked the story, we were panicked about the implications of an early release of the deal. We knew that there would be some initial confusion about why Eclipsys was part of a Novation deal and were not confident that we could convey the benefit convincingly.

But there was no time to control that message. The story was going out almost a week early. Investor confusion could unravel the entire deal before it was even signed.

Hundreds of frenzied calls were exchanged between all parties. A new consensus was quickly reached. In spite of horrendous logistical problems, we would somehow get the final details complete in time for a Thursday morning announcement—just after the leak was to be published.

On Thursday morning, the Neoforma lunch room was decorated profusely with balloons and banners for a big celebration of the formal internal announcement of the merger.

The press announcement had been released prior to the market opening that morning. Anticipation of a huge stock surge, driven by a Novation deal, was trampled soundly by a huge backlash against the Eclipsys announcement.

Everyone hated it.

The investors hated the idea that they had invested in a B2B Internet company that was merging with an old-economy software company. They felt their shot at the astronomical B2B stock returns that other companies had seen was diminished by the merger.

The analysts hated the fact that the merger turned Neoforma into an impure entity. They had made their reputations espousing the wonders of pure Internet e-commerce. This did not fit their vision of a new economy.

The press hated it because it made a better story to hate it.

By the time our company celebration was about to start, Neoforma’s stock had dropped nearly $10 per share. Employees dejectedly trickled into the decorated room. Many didn’t even come. Everyone was angry about everything.

Our execs tried to paint a pretty face onto the ugly reality. I gave a spontaneous speech about the fickle nature of investors and how little they reflected the strength and value of a company. As the crowd filed out of the room, it was clear by the expressions of despair that everyone was getting very tired of fighting . . . for . . . every . . . little . . . bit . . . of . . . ground.

Within a month of the announcement, our stock was down below $7 and still falling.

A year or so later, an analyst told us, “You know, based on what has happened to the pure-play companies versus what has happened to those companies that blended the new and old, I can see now what you were trying to do. It was absolutely the right thing to do. But it was too far ahead of its time.”

I never indulged in fantasies of great wealth again.

But Anni had been well trained by her father, whose family had lived during the Depression . . . Nothing is real until it is real. I begged to differ. Nothing is real until someone imagines it to be real.

I did not want to act on an uncertain future, but neither did I want to deny it. While I have never been one to lean toward extravagance, I couldn’t help having some small fantasies about what I could do with some of this unexpected money.

I imagined creating and funding a guild of talented architects and craftspeople, dedicated to building the beautiful and experimental buildings I had visualized in my design school days. My new business skills could be creatively applied to a profession that I believed was sorely lacking in innovation. I just had to figure out a way to do it without becoming obsessed with or consumed by it.

This seemingly small rift between Anni’s caution and my optimism amplified all the other rifts that had developed over the past decade. I was trying to allow myself some hope that all of the sacrifices we had made would finally be, somehow, justified. She had seen enough hopes suffocated by my pursuit of this venture to be less optimistic.

Neoforma had been working for almost a year to come up with a way to work with Novation, the largest group purchasing organization, the big daddy of GPOs. Their mission was to save hospitals huge amounts of money by aggregating their spending, thereby getting a negotiating edge on the manufacturers.

On the other hand, the manufacturer’s job was to carve out for themselves as much of the healthcare bill as possible. To stay alive, the GPOs needed to carve out a significant part of the savings for themselves too. We walked into one big angry community of sharing with the naïve idea of saving everyone time and money by making the process more efficient.

Of the GPOs, Novation was not only the largest by a hair, but it had a reputation of being one of the most ethical—or maybe just the least belligerent. That kind of fit with Neoforma’s personality. If we could work out a deal with two thousand hospitals at once, our need to waste resources fighting inertia, one hospital at a time, would be nearly eliminated. Our ability to focus would be luxurious.

It was a simple matter of economics. Why should we have a large sales force to sell our services a couple of hospitals at a time, when Novation has already done that job? And why should Novation create an entire technology organization to improve their communication between their suppliers and their member hospitals when technology was not their business?

The GPOs had taken different approaches to fight the broad category they labeled “the dotcoms.” The second largest GPO had decided to aggressively build its own dotcom, investing $50 million to fight us. The third largest GPO had partnered with our second largest competitor, Ventro, which had been a company like us in the laboratory supply space.

Ventro, funded by Kleiner Perkins (KP), had come up with the ultimate way to turn their substantial equity value into astronomical equity value. Their idea was to take a successful public niche company, like one serving the laboratory market, and clone it to serve another niche, like healthcare. The plan was to spin out each company as a new public offering, and so on.

So they reached out and acquired a small, niche medical Internet supply-chain company, Promedix, for $20 million, and became our competitor overnight. At their request, we had spoken with Ventro several times in the past about partnership opportunities. But we were told by their representatives that their investors didn’t like the idea of sharing a large industry that they believed they could dominate. And then there was the ego of their CEO and co-founder, David Perry.

Mr. Perry had painted quite a picture of himself in the media. Thanks to the KP machine, his had been the first B2B supply-chain company to go public. And the company stock had done very, very well. Mr. Perry had taken the bulk of the public credit, becoming something of a rags-to-riches darling in the business press.

Ventro wasn’t satisfied with owning only one company in competion with Neoforma. Our position in the market was too strong. So they orchestrated a major play in the medical supply-chain space. They partnered with the third largest GPO, Broadlane, to create another business chasing Neoforma. With KP’s substantial interest in Medibuy and Ventro, they controlled our three largest competitors.

Novation made their decision in early 1999. They were going to partner with someone, rather than build their own marketplace. They had evaluated more than one hundred candidates for that partnership, but in the end, we like to think it was a cultural issue that swayed their final decision.

Neoforma’s culture, for better and worse, was driven by a standard of cooperation rather than of confrontation. This was ironic, because we had always been seen by the industry players as “an upstart interloper in a system that was already balanced quite well, thank you.”

Novation was a company with a culture similar in many ways to Neoforma, though different in one key way—they moved very, very slowly, by the standards of Neoforma.

It was clear from our first meetings in early 1999 that our com- panies were a good fit for each other. We shared common goals, from a cultural standpoint.

But they needed time—to think about the implications and objectives of a partnership, to discuss it with all of their key members, then make a decision based on the overwhelming consensus of hundreds of hospitals, then send that decision back around for review and consensus.

After all, this is how they made all of their decisions. Making those decisions, carefully and deliberately, was what Novation was all about. Their service was literally about making the decisions on which products to use for a large group of healthcare providers who use those products to save lives every day.

Their decision process dragged on and on. We had meeting after meeting, followed by weeks or months of silence, followed by more meetings. They were in no hurry. They knew that most new healthcare products or services took a decade or so to get into practice.

We weren’t on that kind of schedule. When we became a public company, many analysts had pointed out how beneficial, even critical, it was for Neoforma to partner closely with one or more GPOs. Lever- aging their power was central to maintaining our first mover status.

Novation wasn’t particularly impressed with our IPO success.

They kept saying they were close to making a final decision and they indicated that we were on the short list to be the beneficiary of that decision. But nothing really changed, except our market cap . . .

Which wasn’t really nothing anymore.

Although there had been no public disclosures, we had heard the gossip rampant throughout the healthcare industry that we were close to a deal to partner with Novation, and that Medibuy (or, The Bug, as we called them) was close to a deal to partner with Novation’s primary competitor, Premier, the second largest GPO.

The Bug was still struggling to pull together their IPO. We had been working with Novation in the background for so long that we had taken this pretty much for granted. When Novation continued to drag its feet after our IPO, Bob stepped up as CEO and kicked things into high gear. While Novation was far and away our first choice, due to its great cultural fit and dominant size, we couldn’t afford to just sit back and wait for something to happen.

In February, Bob boldly called the head of Premier and offered $1 billion for Premier’s electronic commerce business. Even for a business that managed about $30 billion worth of spending each year for its members, this was a hard number to ignore.

In contrast to Novation’s reputation as a company driven by process and consensus, Premier had a reputation for forcefulness. Bob, who understood every fiber of this industry, was betting that a decision by Premier would drive the other GPOs into action. This would quickly drive Premier to either us or The Bug.

His gamble was that, if Premier went to The Bug, Novation would accelerate their move to us. Either we would acquire a large number of Premier’s hospital customers or we would weaken KP’s hold on The Bug by substantially increasing Premier’s equity expectations.

Bob’s initiative did instigate a series of hastily assembled meetings between Premier and Neoforma. Premier seemed to take our offer very seriously. While the cultural match between the two companies was far from strong, our common drive toward quick decision was a welcome relief. A deal structure was quickly sent to the lawyers. It looked like Bob’s ploy had worked.

When we thought the deal had been all but formally signed, our execs investigated the housing availability in La Jolla, California, where Premier was headquartered. In addition to beaches and great weather, housing was available for a fraction of the astronomical Bay Area housing costs. They liked that.

Then we heard some disturbing rumors from friends in the industry. Premier’s negotiations with us were a guise.

Premier figured they could trump The Bug by saying that if they didn’t receive a much larger piece of Medibuy than they were going to get from Neoforma, they were going to do a deal with Neoforma. That would practically squash The Bug’s hopes of going public.

And until The Bug caved in, Premier could keep Neoforma from proceeding with Novation, by pretending that they were still proceeding with us as planned. That way, they could announce the merger with The Bug as part of an IPO filing, garnering maximum buzz. Premier and The Bug were convinced that their public valuation would far exceed ours because of the aggressive nature of their mutual businesses.

Hey, it was business. Nasty stuff, but you had to play tough to get on top.

Once we validated these rumors, only a week before the deal was to be publicly announced, we feigned ignorance of the Medibuy deal, calmly stalled all dialog with Premier and notified Novation that we had heard that Premier was going to announce a deal with Medibuy very soon.

Novation may have been the quiet force among these fiercely competitive GPOs, but they were the largest. And their lead against number-two Premier was not very great. They knew a threat when they saw one.

By the time the hastily assembled Premier/Medibuy deal was announced in early March, Novation was wide awake. They were intensifying their talks with us. The preferred outcome to Bob’s plan was working out as planned. However, Novation, in negotiating the best possible deal they could, had made it clear that we had only made it to the short list. We had not yet been selected as the finalist.

As the press speculated about who Neoforma and Novation would partner with, we couldn’t help but look at our future without Novation. If Medibuy were to go public with a huge GPO partner and we did not partner with the only other one that mattered, we could be propelled from the clear market leader to a bit player, overnight.

The tension at Neoforma was very high. We all tried to pursue our assorted tasks with typical enthusiasm, but we knew that our fate was about to change dramatically, one way or the other.

Most of the time though, we assumed that an agreement with Novation was inevitable. That is, until our stock value began to decline. While our stock had climbed as high as $78, it had seemed to settle in the low fifties in early March. However, speculation about how critical a Novation deal was to Neoforma, combined with assorted jitters in the press about how new companies could suffer if the economy slowed down, began to nibble, day by day, at our stock value. By mid-March, our stock had drifted down into the thirties.

Bob had always made sure to emphasize that, as a newly public company, our stock price would be volatile. So we should not be concerned if it went down. We had a lot of work to do before our company grew to fill our market cap.

During our IPO party, Bob did allow a rare moment of indulgence, when he announced: “As of last week, Neoforma now has over a hundred millionaires!” Needless to say, those hundred millionaires cheered heartily at this boast.

Bob didn’t express concern to me about the stock price decline until it dropped into the twenties in late March—the week before our deal with Novation was due to be announced.

“It’s easy to give away a large, but minority, piece of Neoforma to get a deal for a third of the U.S. healthcare market, when our stock is in the fifties or even the forties,” Bob told me. “When it’s in the thirties, our negotiating position becomes much weaker. And in the twenties, it’s nearly impossible.”

For the first and only time, I saw panic in his eyes. For a moment, his innate certainty that his abilities could get him through anything seemed to be faltering. He saw the possibility that we might lose the deal and did not like it.

Once Novation decided to move forward with an Internet initiative, they decided that the best way to ensure quick adoption by hospitals was to incentivize the hospitals that signed up early. The best incentive for the nation’s struggling hospitals was money. And the best way to get that money to the hospitals would be to distribute Neoforma stock to them.

One of Novation’s key missions was to increase the quality of products purchased while saving money for their hospital members. Any money Novation made beyond what was required to support them went back to their members. The only way for all members to fully benefit from an automated commerce system would be to ensure wide adoption of a single solution. Returning money to their membership hospitals was consistent with their way of doing business.

The only problem was that, once they had set their expectation of how much money that would be, it would be hard to adjust to an increasingly lower number.

But the bigger problem was that Novation and their owners felt the need to combine their other software partnerships into one big new solution. They were insistent about it.

Novation had partnered extensively with a healthcare information technology firm called Eclipsys. They had even created a joint venture, HEALTHvision, targeted at helping hospitals set up their own websites. Novation wanted to trump the Medibuy/Premier deal by uniting these companies together into a single initiative. They wanted to add one plus one plus one to make ten.

This arrangement was not popular at Neoforma, to say the least.

First of all, Eclipsys was a large legacy. In other words, it was a maker of cumbersome, difficult-to-update software with well over a thousand employees. They were far from the largest player in health- care information technology (IT), but far from the smallest too.

Most of the software they developed wasn’t Internet software. And its applications served needs across the entire hospital, not just the supply-chain.

But Novation insisted that any solution they embraced needed to accommodate a transition from their older IT initiatives to their new ones. Novation wanted to include them in the deal—or else there would be no deal at all.

I had an aesthetic aversion to the idea of diluting the purity of our Internet model with an older technology solution. On the other hand, I had been in the healthcare market long enough to recognize that the newest solution is not always the one that will be adopted by this sluggish industry. But I knew this would be a pretty gutsy move, putting us in competition with some of the largest IT companies serving healthcare. And that might be fun.

Eclipsys had the challenge of moving from a legacy software provider into an Internet solution provider. Neoforma had the challenge of nudging the Industry’s inertia in our direction. It just might work.

Then I received a call from Debbie, an associate of one of our investors, who had heard that we might be partnering with Eclipsys. Her usually cheerful voice edged with panic, she said, “There’s someone you must speak with before you let this happen!” She asked if we could get together on the East Coast next week.

Jeff and I had a customer visit to New York already scheduled. We agreed to meet her mysterious person there.

When Jeff and I arrived at the trendy New York restaurant, Debbie and Dale were already seated at an appropriately private table. Dale was a friendly man, a decade or two our senior. He seemed like a man who had seen just about everything. He was a senior executive at one of the largest healthcare IT companies and had worked closely with the CEO of Eclipsys many times over the last several decades.

Dale spun a yarn about a man who was simultaneously despised, feared and respected throughout the healthcare industry; a man known—among his employees as well as his competitors—for his viciousness; a man appreciated on Wall Street for his singular focus on the stock value.

“This man will take Neoforma, strip it, and sell it for parts,” Dale said, with conviction. “He lives on the edge. His current company is

struggling with its old, underperforming software. He has been having greater difficulty each quarter meeting his numbers. He is just looking for some fresh meat to chew. And believe me, he’s done this many times before. He is a fierce survivor.”

My heart sunk as I listened to this summary of the man who would become the number-two guy at Neoforma. What would this do to the culture I had so carefully constructed? How could I let this happen?

On the other hand, the way the stock had been sinking, maybe we needed an experienced survivor on our team. Neoforma was going to be the acquirer. Maybe the Neoforma culture was strong enough to survive the influx of an extra thousand or so people. Ultimately, we had little choice in the matter. Our new knowledge would only make my suffering that much more exquisite.

After weeks of intense negotiation, from which I was completely isolated, the day for the public announcement was finally selected.

The press and analysts expressed increasing concern over our lack of a GPO partner. Our stock continued its slide into the low twenties. But we knew that the stock would soar again on the news that we had partnered with the huge GPO. How else could investors react to the announcement of two thousand new hospital customers?

The announcement was scheduled for a Tuesday. The release was being carefully orchestrated. Neoforma, Eclipsys and Novation execs were going to carefully present the new company to key investors, analysts and press contacts. Each company would enthusiastically present a unified vision to its employees.

Then, on the Tuesday a week before the big day, Jeff received a call from a reporter he had spoken with in the past. “I’m doing a story tomorrow on your upcoming merger with Eclipsys,” the reporter said. “I was wondering if you’d like to comment?” He disclosed enough details on the deal structure to verify that someone had leaked every detail of the merger.

In addition to being very angry that someone had leaked the story, we were panicked about the implications of an early release of the deal. We knew that there would be some initial confusion about why Eclipsys was part of a Novation deal and were not confident that we could convey the benefit convincingly.

But there was no time to control that message. The story was going out almost a week early. Investor confusion could unravel the entire deal before it was even signed.

Hundreds of frenzied calls were exchanged between all parties. A new consensus was quickly reached. In spite of horrendous logistical problems, we would somehow get the final details complete in time for a Thursday morning announcement—just after the leak was to be published.

On Thursday morning, the Neoforma lunch room was decorated profusely with balloons and banners for a big celebration of the formal internal announcement of the merger.

The press announcement had been released prior to the market opening that morning. Anticipation of a huge stock surge, driven by a Novation deal, was trampled soundly by a huge backlash against the Eclipsys announcement.

Everyone hated it.

The investors hated the idea that they had invested in a B2B Internet company that was merging with an old-economy software company. They felt their shot at the astronomical B2B stock returns that other companies had seen was diminished by the merger.

The analysts hated the fact that the merger turned Neoforma into an impure entity. They had made their reputations espousing the wonders of pure Internet e-commerce. This did not fit their vision of a new economy.

The press hated it because it made a better story to hate it.

By the time our company celebration was about to start, Neoforma’s stock had dropped nearly $10 per share. Employees dejectedly trickled into the decorated room. Many didn’t even come. Everyone was angry about everything.

Our execs tried to paint a pretty face onto the ugly reality. I gave a spontaneous speech about the fickle nature of investors and how little they reflected the strength and value of a company. As the crowd filed out of the room, it was clear by the expressions of despair that everyone was getting very tired of fighting . . . for . . . every . . . little . . . bit . . . of . . . ground.

Within a month of the announcement, our stock was down below $7 and still falling.

A year or so later, an analyst told us, “You know, based on what has happened to the pure-play companies versus what has happened to those companies that blended the new and old, I can see now what you were trying to do. It was absolutely the right thing to do. But it was too far ahead of its time.”

I never indulged in fantasies of great wealth again.

RSS Feed

RSS Feed