A million bucks was just an entry fee.

Now it was time to play the real game—time to get some real money from a top-tier venture firm and the prestige that goes along with it...

Now it was time to play the real game—time to get some real money from a top-tier venture firm and the prestige that goes along with it...

Board Meeting Minutes

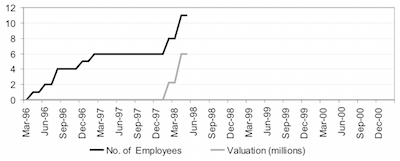

Fundraising: The Board reviewed the terms sheet for the Venrock-led investment totaling $3.65 million at a pre-investment fully diluted valuation of $11 million. The Board approved of the terms sheet and the investment, subject to passing a formal resolution when the papers are drawn up . . .

Neoforma Board Meeting, May 5, 1998

You see, the value of a dollar is, pretty much, a dollar. Except when the dollar is really just the ante to a larger bet. Then it’s somewhat more than a dollar. The greater the bet, the greater the prize.

We knew that we were holding good cards, but outsiders didn’t know who we were yet. So we had to look sharp and confident to potential investors. We had to look comfortable in an unfamiliar world.

Everyone wants to bet on a proven winner. Since neither Jeff nor I were proven winners, Alexander and JP had selected the investors in the previous round carefully. They picked people who had made successful bets before.

Then they began to groom us for our new roles. They introduced Jeff and me to other entrepreneurs, teasing us with offhand stories about how these guys had just sold their companies for a fortune, or were about to. We were being trained to project the image that we knew without question we were Players.

Frankly, I was more interested in figuring out how best to spend the million bucks we had. I just wanted to run the business, to help and excite more people by making innovative and valuable software. The rest was just a distraction to me. That’s why Jeff made a better front man. He enjoyed the challenge of playing his part convincingly. Little did we know that we would need him to leverage this talent almost continuously for years to come.

Jeff has an amazing ability to instantaneously integrate new information into his vocabulary. He was able to take the most technical or esoteric jargon from one meeting and correctly use it at the next. I knew him well enough to know that he was sometimes winging it, but he became very adept at communicating with even the most sophisticated investors and business partners.

Once we moved beyond angel investors, my role the investment process became largely limited to helping prepare presentations. I was okay with this role, because it gave me time to focus on operations.

Though I was trying to keep my attention on running the company, I must admit that it was pretty interesting watching Alexander and JP work the Scene.

They knew that the next funding round would need to come from a venture capital firm that other firms would blindly follow in future, much larger funding rounds. And so on. The venture firms that are followed blindly are called top-tier. There is no hard and fast rule for who is top-tier, who is second-tier and so on, but there are a handful of firms that are universally recognized as the top of the top-tier.

Alexander and JP made sure that at least one of the top-tier venture firms was represented on our list of investors, via Bret Emery, whom we had not met, but who had invested heavily in our previous round. Bret was a free-lance investor, but he was also connected to the prestigious venture firm, Venrock. As the venture arm of the Rockefeller family, Venrock was definitely near the top of the top tier, although their East Coast origin made them somewhat less sexy than the local Sand Hill Road venture firms.

Although Bret was a carefully selected investor, Venrock was not necessarily our venture firm of choice. Alexander and JP looked at it this way: either we would shop the top Sand Hill Road venture firms by dropping the old-money Venrock name, or we would shop these Sand Hill Road firms and then go back to Venrock, positioning these upstart venture firms against them. Or both. They always had multiple positive scenarios for each decision they made. The direction they pursued would be based on where the quickest valuation ramp-up could be achieved.

The fact that the top-tier venture firms funded only one in a thousand of the businesses they reviewed was irrelevant to Alexander and JP. The Internet was hot. Neoforma was an Internet company serving a huge market. And most of all, Neoforma had been vetted by Alexander and JP. Why wouldn’t venture firms fight for the privilege to bet on us?

The firm they really wanted was Kleiner Perkins Caufield & Byers (KP), the current number-one VC darling of the Valley. In the intensifying stock market of mid-1998, it was generally believed that any company funded by KP was almost guaranteed to be successful, or at least famous. And when it came to raising money, that was pretty much the same thing.

Alexander and JP were staging everything to increase the chances of getting Neoforma funded by KP. If they succeeded, in addition to their increased chance of financial reward from Neoforma, their position as super angels would be greatly enhanced. They would get access to more and better deals. And they would be able to get bigger pieces of these future deals. That’s how things worked.

So the idea was to create maximum buzz by visiting four or five top-tier venture firms, all in one week. We knew that these firms communicated with each other regularly. They would quickly find out what other firms we were meeting with. It was in the interest of these friendly competitors to regularly communicate with each other about new deals. In order to keep their top-tier status, these firms needed some form of the tacit consensus as to what was hot and what was not. This way, unpopular deals—those that might have difficulty receiving top-tier money in the future—could be delegated to the lower tiers.

Alexander and JP coached us extensively on how we were expected to behave. We would only meet with the venture firms after they had expressed serious interest in funding us and had set up a presentation to at least one key partner in the firm. We would then give a concise presentation and answer questions about the business. We were not to discuss the deal. All of the crucial details of a funding deal would be done by Alexander and JP. To keep us out of this area they played to our egos. “You have much too much to do as it is just running the business. You do what you do best and let us do what we do best. Your time is too important to be mixed up in funding issues.”

These presentations did take up quite a bit of our time though. We went through endless revisions to our investor presentation. Alexander and JP were never happy. We always had too many slides about the product. We’d take out slides. Then we didn’t have enough financial information. They’d give us some new things to add. Then we had too many slides again. We’d take out some more. They’d add some in. In the end, there was very little information about what we were doing. We could have been anybody doing just about anything. But we were showing that our market was very large.

While Alexander and JP were trying to make us presentable, they were working the phones, leveraging their extensive network to carefully orchestrate a week of meetings. They gave us upbeat assessments of their progress, but offered few details. We figured that, with their prestige and our business model, they would have no problem getting us in front of KP.

But that was not to be. For some reason they were not interested in our space. We didn’t fit into the kind of market they wished to pursue. Or so Alexander and JP told us. Jeff and I shared a hard-to-justify belief that there was something more at work here—that perhaps Alexander and JP were not as well-connected as we had thought. We got a bit nervous. However, they did successfully schedule meetings with several well- known, top-tier firms.

The big week had come. The show was on.

Jeff and I showed up at each meeting. We talked the talk. We walked the walk. We acted confident. We confidently acted.

But in each debriefing with Alexander and JP, we became less confident. While our story was well-received, our space was — well, unproven. Like it or not, healthcare wasn’t a very exciting market. Ideas targeting consumers were much more familiar to investors. While there was indeed much buzz about the potential of business-to- business companies, there hadn’t been any successful B2B IPOs yet.

Alexander and JP played to each firm’s sense of domination. “Now, we are only raising a few million dollars, so we need to know whether you would lead the round with the largest investment, or if you simply want to follow another top-tier firm with a smaller investment.”

So no firm, except KP, was outright dismissing us. Most of the firms expressed an interest in taking part in a round. They just wanted someone else to take the lead. They needed more time to think about a deal like ours.

It became clear that, while several firms were considering us, nobody was willing to quickly commit to take the lead. This was a common problem for young companies. VCs love the idea of leading investment rounds — once another firm has said that they are willing to lead it.

Alexander and JP wanted to make sure that word did not have time to spread that Neoforma wasn’t likely to be immediately grabbed by one of these prestigious firms. So they implemented phase two of their plan.

They called Venrock.

They implied that this hot Valley company was about to be funded, but since Bret had been in the previous round, we wanted to let them look at the deal before closing it with someone else. They’d have to act fast though. We expected our first term sheet that week. (A term sheet is what VCs give you as a serious expression of their interest.)

Suitably stirred up by the idea of losing a great deal to a Valley firm, Venrock quickly decided to take an unprecedented action. They would have us present to their entire partner team in a single meeting. It just so happened that the New York partners were meeting at their Sand Hill office the following week. Alexander told them, “Well, we can’t guarantee where we’d be in the process with other firms, but we can make sure that we don’t sign with anyone else until you look at this. Since this would require a quick decision, it would be best if your team met in the Neoforma offices, so that we can make sure that anyone you need to speak with will be immediately available.”

To ensure that their statement about expecting a term sheet from another firm was accurate, Alexander and JP went back to the VCs we had met with and let them know that the potential for them to lead a deal was nearly gone. In fact, Venrock had a reputation for funding large deals, so it was probable that they would take the entire deal. It wasn’t likely there would be room left for any other VC to participate.

Under this pressure, one of the firms decided to rush a term sheet to us after all.

At this point, the Neoforma offices were buzzing with energy. We were growing into an increasing number of rooms in the office suite. Each room was hot and muggy from hosting more people and computers than the air conditioning was designed to handle. Everyone was busy and excited about what they were doing.

Alexander and JP knew this. They knew how contagious the startup environment could be. That’s why they staged the meeting with Venrock to be held in the small, glass-enclosed conference room that we shared with other companies in the suite. We met the conservatively suited partners in our shared lobby, gave them a quick tour of our cramped offices, and sat them down in the unadorned conference room.

Playing the part of a company in a hurry to get to the point, we gave a much less formal presentation of Neoforma than we had been giving. Somehow the contrast between the formality of their dress and the informality of our presentation and offices spawned an atmosphere of candor. They were open with us, to a degree. We were open with them, to a degree. Unlike our other presentations, Jeff and I were truly comfortable in the meeting.

Maybe it was the brilliant staging by JP and Alexander. Maybe it was the rare presence of all of the decision-makers in one room. Maybe it was the electric sensation of a start-up, created by our energetic staff, buzzing past the conference room windows. Maybe it was some odd compatibility between their conservative East Coast nature and the conservative nature of healthcare. Maybe Jeff was being more charming than ever. Maybe my hair wasn’t sticking up as much as usual. For whatever reason, the meeting was a success. And everyone knew it.

The meeting went on far longer than planned. When it was clear that it had accomplished its objective, JP and Alexander exchanged a subtle signal. Alexander said, “Okay. So now that we are all in love with each other, let’s get on to the next step.”

Ray, the lead Venrock partner said, “Well, this deal looks very good to us. We’ll discuss it between us in our offices this afternoon and get back to you.”

Alexander displayed exasperation and said, “Who else needs to be part of this decision besides all of you?”

Ray said, “Nobody.”

Alexander quickly said, “Then you have everything you need right here. We thought you came here to seriously evaluate this deal . . .”

He glanced at JP, as if to say, Wasn’t that what you thought they were here for? “Come on, guys. What’s it going to be? Are you going to do this deal or not? Let’s not waste anyone’s time on this. We’ll just step out of the room and you let us know when you’ve made a decision.”

Ray paused, clearly stunned by this tactic. He looked at his team with an expression that said, Sheesh! These Silicon Valley boys sure don’t play by the rules. But he said aloud, “Okay. Give us some time to talk about this.”

Jeff and I walked out of the room flabbergasted. This took some nerve. After all, our other offer was by no means assured. What would we do if this fell through? We paced in our offices, listening to Alexander and JP discuss our position. They were optimistic. They felt that their move to force a decision had a fair chance of working. I could see that they were nervous, but I could also see that this kind of moment was what they lived for. They were high on buzz.

Not ten minutes after leaving the room, Bret came to call us back to the room. Because of the short duration of their meeting, we figured we were about to be dismissed.

Ray said, “Well, we have never made a decision about any deal in a week . . . much less ten minutes.” His team laughed. A quick consensus was clearly something of an oxymoron for this group. “So it is quite startling for me to be here saying, Yes indeed. We would like to do a deal with you . . . pending due diligence. We feel very good about this company. We’ll get you a term sheet tomorrow.”

And just like that Neoforma became a Player. With a name like Venrock behind us, we would be a formidable company. And another three-and-a-half-million dollars could take us to previously unimagined places.

We were excited to tell our early investors about the deal, now that we had doubled the value of their investments since the previous round, completed just two months ago.

Jack, our lawyer and first investor, was even more effusive than usual. He acted like a proud papa, telling us that we wouldn’t need him any more now that we were in the big leagues.

To our surprise, our angel investors, Wally and Denis, were less enthusiastic.

They were happy to see their investments grow, but they were unhappy that we hadn’t included them in more of the VC selection process. They hadn’t told us they wanted to play a part there, but they clearly hadn’t expected things to move so quickly past them. They emphasized our need to be cautious. “Alexander and JP are impressive fundraisers,” they warned us again. “But they are not working for you the way we have been. If you are not careful, they will eat you up and spit you out of your own firm.”

We had been so transfixed by the magic of Alexander and JP—and so thrilled by the investment—that we were stunned to think that Wally and Denis might not think their results were so great. We told them not to worry, we could take care of ourselves.

As the details contained in the final paperwork for the funding round were revealed and discussed, Wally and Denis became increasingly agitated. Just five months earlier, they had decided to invest in Neoforma. They had each joined our Board with the idea that they would play an active and primary role in the company’s growth for some time to come. Now things were different. When a VC invests in a company, it is assumed that they will appoint someone to represent them on the company’s Board of Directors. They selected Bret Emery. They also insisted that, since Alexander and JP brought the deal to Venrock, one of them needed to have a Board position to represent the previous investors. Everyone agreed that a board larger than five members for a company as small as ours didn’t make sense. So, if Jeff and I were both going to remain on the Board, that left only one position for our early investors. Of Wally, Denis and Jack, only one could remain on the Board. Two would have to step down.

Jack had already made it clear that he was ready to step down, but Wally and Denis were not so compliant. Wally was inherently wary of quick decisions. And Denis didn’t trust the motives of Alexander and JP. He still mourned the fact that he had given up control of the Board of a company he had co-founded long ago.

Denis expressed his concerns in a message to the Board.

We knew that we were holding good cards, but outsiders didn’t know who we were yet. So we had to look sharp and confident to potential investors. We had to look comfortable in an unfamiliar world.

Everyone wants to bet on a proven winner. Since neither Jeff nor I were proven winners, Alexander and JP had selected the investors in the previous round carefully. They picked people who had made successful bets before.

Then they began to groom us for our new roles. They introduced Jeff and me to other entrepreneurs, teasing us with offhand stories about how these guys had just sold their companies for a fortune, or were about to. We were being trained to project the image that we knew without question we were Players.

Frankly, I was more interested in figuring out how best to spend the million bucks we had. I just wanted to run the business, to help and excite more people by making innovative and valuable software. The rest was just a distraction to me. That’s why Jeff made a better front man. He enjoyed the challenge of playing his part convincingly. Little did we know that we would need him to leverage this talent almost continuously for years to come.

Jeff has an amazing ability to instantaneously integrate new information into his vocabulary. He was able to take the most technical or esoteric jargon from one meeting and correctly use it at the next. I knew him well enough to know that he was sometimes winging it, but he became very adept at communicating with even the most sophisticated investors and business partners.

Once we moved beyond angel investors, my role the investment process became largely limited to helping prepare presentations. I was okay with this role, because it gave me time to focus on operations.

Though I was trying to keep my attention on running the company, I must admit that it was pretty interesting watching Alexander and JP work the Scene.

They knew that the next funding round would need to come from a venture capital firm that other firms would blindly follow in future, much larger funding rounds. And so on. The venture firms that are followed blindly are called top-tier. There is no hard and fast rule for who is top-tier, who is second-tier and so on, but there are a handful of firms that are universally recognized as the top of the top-tier.

Alexander and JP made sure that at least one of the top-tier venture firms was represented on our list of investors, via Bret Emery, whom we had not met, but who had invested heavily in our previous round. Bret was a free-lance investor, but he was also connected to the prestigious venture firm, Venrock. As the venture arm of the Rockefeller family, Venrock was definitely near the top of the top tier, although their East Coast origin made them somewhat less sexy than the local Sand Hill Road venture firms.

Although Bret was a carefully selected investor, Venrock was not necessarily our venture firm of choice. Alexander and JP looked at it this way: either we would shop the top Sand Hill Road venture firms by dropping the old-money Venrock name, or we would shop these Sand Hill Road firms and then go back to Venrock, positioning these upstart venture firms against them. Or both. They always had multiple positive scenarios for each decision they made. The direction they pursued would be based on where the quickest valuation ramp-up could be achieved.

The fact that the top-tier venture firms funded only one in a thousand of the businesses they reviewed was irrelevant to Alexander and JP. The Internet was hot. Neoforma was an Internet company serving a huge market. And most of all, Neoforma had been vetted by Alexander and JP. Why wouldn’t venture firms fight for the privilege to bet on us?

The firm they really wanted was Kleiner Perkins Caufield & Byers (KP), the current number-one VC darling of the Valley. In the intensifying stock market of mid-1998, it was generally believed that any company funded by KP was almost guaranteed to be successful, or at least famous. And when it came to raising money, that was pretty much the same thing.

Alexander and JP were staging everything to increase the chances of getting Neoforma funded by KP. If they succeeded, in addition to their increased chance of financial reward from Neoforma, their position as super angels would be greatly enhanced. They would get access to more and better deals. And they would be able to get bigger pieces of these future deals. That’s how things worked.

So the idea was to create maximum buzz by visiting four or five top-tier venture firms, all in one week. We knew that these firms communicated with each other regularly. They would quickly find out what other firms we were meeting with. It was in the interest of these friendly competitors to regularly communicate with each other about new deals. In order to keep their top-tier status, these firms needed some form of the tacit consensus as to what was hot and what was not. This way, unpopular deals—those that might have difficulty receiving top-tier money in the future—could be delegated to the lower tiers.

Alexander and JP coached us extensively on how we were expected to behave. We would only meet with the venture firms after they had expressed serious interest in funding us and had set up a presentation to at least one key partner in the firm. We would then give a concise presentation and answer questions about the business. We were not to discuss the deal. All of the crucial details of a funding deal would be done by Alexander and JP. To keep us out of this area they played to our egos. “You have much too much to do as it is just running the business. You do what you do best and let us do what we do best. Your time is too important to be mixed up in funding issues.”

These presentations did take up quite a bit of our time though. We went through endless revisions to our investor presentation. Alexander and JP were never happy. We always had too many slides about the product. We’d take out slides. Then we didn’t have enough financial information. They’d give us some new things to add. Then we had too many slides again. We’d take out some more. They’d add some in. In the end, there was very little information about what we were doing. We could have been anybody doing just about anything. But we were showing that our market was very large.

While Alexander and JP were trying to make us presentable, they were working the phones, leveraging their extensive network to carefully orchestrate a week of meetings. They gave us upbeat assessments of their progress, but offered few details. We figured that, with their prestige and our business model, they would have no problem getting us in front of KP.

But that was not to be. For some reason they were not interested in our space. We didn’t fit into the kind of market they wished to pursue. Or so Alexander and JP told us. Jeff and I shared a hard-to-justify belief that there was something more at work here—that perhaps Alexander and JP were not as well-connected as we had thought. We got a bit nervous. However, they did successfully schedule meetings with several well- known, top-tier firms.

The big week had come. The show was on.

Jeff and I showed up at each meeting. We talked the talk. We walked the walk. We acted confident. We confidently acted.

But in each debriefing with Alexander and JP, we became less confident. While our story was well-received, our space was — well, unproven. Like it or not, healthcare wasn’t a very exciting market. Ideas targeting consumers were much more familiar to investors. While there was indeed much buzz about the potential of business-to- business companies, there hadn’t been any successful B2B IPOs yet.

Alexander and JP played to each firm’s sense of domination. “Now, we are only raising a few million dollars, so we need to know whether you would lead the round with the largest investment, or if you simply want to follow another top-tier firm with a smaller investment.”

So no firm, except KP, was outright dismissing us. Most of the firms expressed an interest in taking part in a round. They just wanted someone else to take the lead. They needed more time to think about a deal like ours.

It became clear that, while several firms were considering us, nobody was willing to quickly commit to take the lead. This was a common problem for young companies. VCs love the idea of leading investment rounds — once another firm has said that they are willing to lead it.

Alexander and JP wanted to make sure that word did not have time to spread that Neoforma wasn’t likely to be immediately grabbed by one of these prestigious firms. So they implemented phase two of their plan.

They called Venrock.

They implied that this hot Valley company was about to be funded, but since Bret had been in the previous round, we wanted to let them look at the deal before closing it with someone else. They’d have to act fast though. We expected our first term sheet that week. (A term sheet is what VCs give you as a serious expression of their interest.)

Suitably stirred up by the idea of losing a great deal to a Valley firm, Venrock quickly decided to take an unprecedented action. They would have us present to their entire partner team in a single meeting. It just so happened that the New York partners were meeting at their Sand Hill office the following week. Alexander told them, “Well, we can’t guarantee where we’d be in the process with other firms, but we can make sure that we don’t sign with anyone else until you look at this. Since this would require a quick decision, it would be best if your team met in the Neoforma offices, so that we can make sure that anyone you need to speak with will be immediately available.”

To ensure that their statement about expecting a term sheet from another firm was accurate, Alexander and JP went back to the VCs we had met with and let them know that the potential for them to lead a deal was nearly gone. In fact, Venrock had a reputation for funding large deals, so it was probable that they would take the entire deal. It wasn’t likely there would be room left for any other VC to participate.

Under this pressure, one of the firms decided to rush a term sheet to us after all.

At this point, the Neoforma offices were buzzing with energy. We were growing into an increasing number of rooms in the office suite. Each room was hot and muggy from hosting more people and computers than the air conditioning was designed to handle. Everyone was busy and excited about what they were doing.

Alexander and JP knew this. They knew how contagious the startup environment could be. That’s why they staged the meeting with Venrock to be held in the small, glass-enclosed conference room that we shared with other companies in the suite. We met the conservatively suited partners in our shared lobby, gave them a quick tour of our cramped offices, and sat them down in the unadorned conference room.

Playing the part of a company in a hurry to get to the point, we gave a much less formal presentation of Neoforma than we had been giving. Somehow the contrast between the formality of their dress and the informality of our presentation and offices spawned an atmosphere of candor. They were open with us, to a degree. We were open with them, to a degree. Unlike our other presentations, Jeff and I were truly comfortable in the meeting.

Maybe it was the brilliant staging by JP and Alexander. Maybe it was the rare presence of all of the decision-makers in one room. Maybe it was the electric sensation of a start-up, created by our energetic staff, buzzing past the conference room windows. Maybe it was some odd compatibility between their conservative East Coast nature and the conservative nature of healthcare. Maybe Jeff was being more charming than ever. Maybe my hair wasn’t sticking up as much as usual. For whatever reason, the meeting was a success. And everyone knew it.

The meeting went on far longer than planned. When it was clear that it had accomplished its objective, JP and Alexander exchanged a subtle signal. Alexander said, “Okay. So now that we are all in love with each other, let’s get on to the next step.”

Ray, the lead Venrock partner said, “Well, this deal looks very good to us. We’ll discuss it between us in our offices this afternoon and get back to you.”

Alexander displayed exasperation and said, “Who else needs to be part of this decision besides all of you?”

Ray said, “Nobody.”

Alexander quickly said, “Then you have everything you need right here. We thought you came here to seriously evaluate this deal . . .”

He glanced at JP, as if to say, Wasn’t that what you thought they were here for? “Come on, guys. What’s it going to be? Are you going to do this deal or not? Let’s not waste anyone’s time on this. We’ll just step out of the room and you let us know when you’ve made a decision.”

Ray paused, clearly stunned by this tactic. He looked at his team with an expression that said, Sheesh! These Silicon Valley boys sure don’t play by the rules. But he said aloud, “Okay. Give us some time to talk about this.”

Jeff and I walked out of the room flabbergasted. This took some nerve. After all, our other offer was by no means assured. What would we do if this fell through? We paced in our offices, listening to Alexander and JP discuss our position. They were optimistic. They felt that their move to force a decision had a fair chance of working. I could see that they were nervous, but I could also see that this kind of moment was what they lived for. They were high on buzz.

Not ten minutes after leaving the room, Bret came to call us back to the room. Because of the short duration of their meeting, we figured we were about to be dismissed.

Ray said, “Well, we have never made a decision about any deal in a week . . . much less ten minutes.” His team laughed. A quick consensus was clearly something of an oxymoron for this group. “So it is quite startling for me to be here saying, Yes indeed. We would like to do a deal with you . . . pending due diligence. We feel very good about this company. We’ll get you a term sheet tomorrow.”

And just like that Neoforma became a Player. With a name like Venrock behind us, we would be a formidable company. And another three-and-a-half-million dollars could take us to previously unimagined places.

We were excited to tell our early investors about the deal, now that we had doubled the value of their investments since the previous round, completed just two months ago.

Jack, our lawyer and first investor, was even more effusive than usual. He acted like a proud papa, telling us that we wouldn’t need him any more now that we were in the big leagues.

To our surprise, our angel investors, Wally and Denis, were less enthusiastic.

They were happy to see their investments grow, but they were unhappy that we hadn’t included them in more of the VC selection process. They hadn’t told us they wanted to play a part there, but they clearly hadn’t expected things to move so quickly past them. They emphasized our need to be cautious. “Alexander and JP are impressive fundraisers,” they warned us again. “But they are not working for you the way we have been. If you are not careful, they will eat you up and spit you out of your own firm.”

We had been so transfixed by the magic of Alexander and JP—and so thrilled by the investment—that we were stunned to think that Wally and Denis might not think their results were so great. We told them not to worry, we could take care of ourselves.

As the details contained in the final paperwork for the funding round were revealed and discussed, Wally and Denis became increasingly agitated. Just five months earlier, they had decided to invest in Neoforma. They had each joined our Board with the idea that they would play an active and primary role in the company’s growth for some time to come. Now things were different. When a VC invests in a company, it is assumed that they will appoint someone to represent them on the company’s Board of Directors. They selected Bret Emery. They also insisted that, since Alexander and JP brought the deal to Venrock, one of them needed to have a Board position to represent the previous investors. Everyone agreed that a board larger than five members for a company as small as ours didn’t make sense. So, if Jeff and I were both going to remain on the Board, that left only one position for our early investors. Of Wally, Denis and Jack, only one could remain on the Board. Two would have to step down.

Jack had already made it clear that he was ready to step down, but Wally and Denis were not so compliant. Wally was inherently wary of quick decisions. And Denis didn’t trust the motives of Alexander and JP. He still mourned the fact that he had given up control of the Board of a company he had co-founded long ago.

Denis expressed his concerns in a message to the Board.

Questions: Just who is the new Board member Bret Emery? What other boards does he serve on? What is his reputation?

He was a senior VP at Oracle (known for a heartless management style), worked at another company known for its sloppy management style, and another company known as a top-quality firm of decisive, but somewhat arrogant and opinionated consultants to senior management.

There should be a frank discussion about CEO position and surprisingly there has not been (and should be soon). On paper, Jeff’s background is not what VC’s are looking for—they may like him so much that is no problem, or there may be another agenda.

If new CEO comes in, then CEO gets position and Board cannot have 3 management members on board, so Wayne or Jeff loses a seat. The founders would be down to 1 vote out of 5.

Bret Emery would be in full control when this happens.

Alexander made it clear to Jeff and me that he did not want Denis to remain on the Board. He used the excuse that it looked better to have an M.D. on the Board (which meant Wally), but it was clear that he did not particularly value Denis’s previous accomplishments and conservative style. He had founded a company, yes, but what use was that to us now? He wasn’t a Player.

So Jack and Denis left the Board. Wally, Jeff and I remained on the Board. And JP and Bret joined the Board. Sadly, we didn’t hear much from Denis after that. JP was active off and on, advising us in certain issues.

And Bret didn’t really pay much attention to us until the IPO heat awoke him a year later. We were generally happy about that, since we had heard horror stories about overly intrusive VCs. We figured that he just trusted us to do what needed to be done. Later, we would get to know him very well.

So Jack and Denis left the Board. Wally, Jeff and I remained on the Board. And JP and Bret joined the Board. Sadly, we didn’t hear much from Denis after that. JP was active off and on, advising us in certain issues.

And Bret didn’t really pay much attention to us until the IPO heat awoke him a year later. We were generally happy about that, since we had heard horror stories about overly intrusive VCs. We figured that he just trusted us to do what needed to be done. Later, we would get to know him very well.

RSS Feed

RSS Feed