. . . Of the two start-ups [Neoforma and Medibuy], Neoforma has the more technically sophisticated website . . . Neoforma seems to have better technology and stronger managers than its rival . . .

Forbes Magazine, September 1999

Money brought everything to the surface.

Everything had been set up. The pieces were falling into place. The press was talking about us. Investors were buzzing about us. Wall Street was in a frenzy of excitement. Money was breeding money, and its offspring were fertile at birth...

Everything had been set up. The pieces were falling into place. The press was talking about us. Investors were buzzing about us. Wall Street was in a frenzy of excitement. Money was breeding money, and its offspring were fertile at birth...

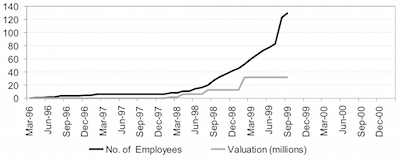

As Neoforma prepared for its public debut, the legal and accounting bills were becoming astronomical. I watched in wonder as flocks of unfamiliar suits moved in and out of our offices each day.

To ensure that nobody doubted that Bob was in firm control of the company, I stayed very much in the background. Jeff was equally deferential toward Bob. He was very pleased to be out of the spotlight. Our burdens lightened, Jeff and I were actually starting to speak to each other again. We made it clear to Bob that we were happy to help out wherever we could.

In order to create the biggest buzz, the IPO production consisted of three primary parts. First, the company needed to get bigger, stronger and better. We were building the strongest team possible to accomplish this task. Second, we needed to build an even stronger financial foundation. If we brought in more money prior to a public offering, we would be much less vulnerable to an unpredictable future. We figured that--oh, about $70 million—would do the trick. And, if that money came from strong corporate partners, we would create a security buffer around our relatively new enterprise. Third, we had to select a strong banker to usher us through the IPO process.

For the most part, Jeff and I were helping Bob along the lines we had established early on: Jeff assisted Bob with tasks involving investors and I helped with tasks involving personnel and operations. However, these areas began to overlap heavily as we lined up our strategic funding round.

Neoforma’s place in the limelight gave us the previously unimaginable power to focus more on who we would allow to invest rather than who we could convince to invest. In July, Chemdex, the Kleiner Perkins (KP) –backed B2B company, had made a very successful IPO debut. Chemdex became the overnight benchmark for valuing new B2B companies. Their company had a huge valuation and their market in laboratory products was very small, compared to the healthcare market that Neoforma dominated. With Neoforma’s IPO imminent, just about any corporate investor would jump at the nearly certain chance to double or quadruple their money in six months or so.

We created a dream list of the types of strategic investors we wanted to have in our final pre-IPO investment round. First, we wanted at least one solid, household-name company to invest in us. Gaining the confidence of well-known companies would help us project a very good image.

Second, we wanted to get support from an established software technology company. There had been much speculation in the press that the big software companies were aggressively targeting the markets of some of the new B2B companies. We wanted to distance ourselves from the new software technology companies that might easily be made obsolete by established players.

Finally, we wanted some of the big suppliers in healthcare to invest in us. By now, everyone knew that one of the biggest uncertainties in the business models of B2B companies was what the established suppliers might do to resist the newcomers. It makes it very difficult to sell stuff when the seller refuses to sell.

The generic identities of the companies on our list were gradually replaced with actual names. Assorted relationships that Neoforma had already established quickly yielded leads on interested corporate investors.

Dell Computer Corporation had a strategic investment fund that was interested in leading the round. With Dell’s reputation for innovative business management at its peak, adding them to our list would certainly achieve our goal of being associated with a household name.

SAP America, the U.S. branch of the huge enterprise software company, seemed to be a perfect choice as a software technology investor.

Their software had a substantial presence in the offices of healthcare suppliers, as well as at large hospital systems. We had been partnering successfully with SAP for several months. While they didn’t have a fund dedicated to the pursuit of strategic investments, they were very interested in pursuing an investment in us.

We hoped to get an investor in each of three supplier categories: medical equipment, medical supplies and medical distribution. Other than pharmaceuticals, which was an area we weren’t interested in pursuing in the near future, these were the three big areas in healthcare.

In our early days, we had found General Electric to be one of the most stubborn medical equipment manufacturers for us to deal with. Their aggressive pursuit of dominance of each of their markets created such a strong outward force that their corporate policies were nearly impenetrable. They did not like the idea of allowing upstart companies to get so much as a foothold in their domain.

Though we had been cautiously probed by some of their largest competitors, GE had shut its doors tightly on us. They made it clear to us that they believed there was nothing we could do that they couldn’t do better on their own.

Then, as we were building up to the IPO, GE called us. They wanted to talk. One of the lead managers in their strategic investment fund had seen Bob speak at an investor conference and reported that Neoforma held far and away the most exciting potential of any company he’d heard about at the show. That got the attention of GE management.

Healthcare was a large part of GE’s business and yielded among the most consistent and lucrative profits. The margin—the amount of money made on each sale—was very high in healthcare equipment. If there were a company out there that might threaten those margins, and if that company were to acquire enough assets, well—that would be very bad for executive bonuses.

So, GE had done some very serious investigation of the increasing numbers of B2B healthcare companies and had come to the conclusion that Neoforma was simultaneously the strongest and least threatening of the bunch. At least that’s what they told us.

We certainly couldn’t argue with their conclusion. We were the strongest and we had always held a participatory, rather than confrontational, position with suppliers. Our main competitor, Medibuy, was openly and foolishly promoting a let’s band together and screw the manufacturers message to potential hospital customers.

We had no doubt that GE considered us the lesser of evils, rather than the greater of opportunities—but, hey, they were GE, and GE was the undisputed U.S. leader in healthcare equipment.

In an initial meeting with us, the GE representatives had come in with a very condescending attitude. When we made it apparent that we didn’t consider them much more important than the other ten thousand medical manufacturers, they were visibly startled. The tone of the conversation changed quickly. After a few meetings, they informed us that they would be happy to extend to us the privilege of consideration for investment. And we told them that we’d be happy to listen to what they had to say.

GE was to healthcare equipment what Johnson & Johnson was to healthcare supplies. And it just so happened that J&J was interested in us too — though for a very different reason. Whereas GE saw us as a threat, J&J saw us as an opportunity. They did not like what the group purchasing organizations had done to their margins in the supplies markets. They wanted to crush the GPOs. They saw Neoforma as a chance to do just that. But that meant, they’d need some control over us. When they expressed their interest in investing, we said okay.

The largest distributor of healthcare supplies was Cardinal. When Bob accepted the top job at Neoforma, he had been certain that Cardinal would be enthusiastic about investing in our strategic round. But when Bob’s former boss at Cardinal decided that Bob had betrayed the company by leaving, that was no longer a possibility. Fortunately, there were several other large distributors with which we were on friendly terms, so we discussed strategic investment possibilities with them. Two of them thought this was a good idea.

Several of our previous venture firms and many new ones wanted to play too. Jeff and I were both receiving calls from venture firms all over the country, espousing their connections and expertise, asking to be considered for participation in the funding round. They were offering to put millions in, no questions asked.

One of the calls was from Jack, our mentor and first attorney. He told me that a partner from one of the first venture firms we had

made a presentation to, two years earlier, had called him to ask “a big favor.”

He wanted Jack to convince Jeff and me to include his firm in the round.

I could tell that Jack was perversely thrilled to deliver this message. I remembered our presentation to this guy very well. He had been among the most dismissive and condescending VCs we had met. And that was saying a lot.

Jack knew our answer, but wanted to hear us say it. He had been so enthusiastic about us at the time and had been very upset that the VCs didn’t see why. He had taken it personally. It was a pleasure for him to deliver our answer personally.

Everything seemed to be lining up nicely. This list of investors was more than we could have hoped for. I was very excited by the knowledge that our team of partners could not possibly be topped by Medibuy, however powerful their keiretsu was.

Keiretsu is a term borrowed from the Japanese. It refers to a conglomerate of businesses linked together by a common financial interest. The term had become associated with KP because of the way they were leveraging the power of companies they’d previously invested in to support their newer investments. We knew they were trying very hard to gain ground on us. KP was not used to settling for second place.

With such a powerful list of investors lining up behind Neoforma, all we had to do was to work out the details. In a few short months, we needed to get them all to agree to a set of financial terms that were favorable to us. The higher our valuation, the lower our dilution would be and the more money our investors could recover after the IPO.

To be continued...

To ensure that nobody doubted that Bob was in firm control of the company, I stayed very much in the background. Jeff was equally deferential toward Bob. He was very pleased to be out of the spotlight. Our burdens lightened, Jeff and I were actually starting to speak to each other again. We made it clear to Bob that we were happy to help out wherever we could.

In order to create the biggest buzz, the IPO production consisted of three primary parts. First, the company needed to get bigger, stronger and better. We were building the strongest team possible to accomplish this task. Second, we needed to build an even stronger financial foundation. If we brought in more money prior to a public offering, we would be much less vulnerable to an unpredictable future. We figured that--oh, about $70 million—would do the trick. And, if that money came from strong corporate partners, we would create a security buffer around our relatively new enterprise. Third, we had to select a strong banker to usher us through the IPO process.

For the most part, Jeff and I were helping Bob along the lines we had established early on: Jeff assisted Bob with tasks involving investors and I helped with tasks involving personnel and operations. However, these areas began to overlap heavily as we lined up our strategic funding round.

Neoforma’s place in the limelight gave us the previously unimaginable power to focus more on who we would allow to invest rather than who we could convince to invest. In July, Chemdex, the Kleiner Perkins (KP) –backed B2B company, had made a very successful IPO debut. Chemdex became the overnight benchmark for valuing new B2B companies. Their company had a huge valuation and their market in laboratory products was very small, compared to the healthcare market that Neoforma dominated. With Neoforma’s IPO imminent, just about any corporate investor would jump at the nearly certain chance to double or quadruple their money in six months or so.

We created a dream list of the types of strategic investors we wanted to have in our final pre-IPO investment round. First, we wanted at least one solid, household-name company to invest in us. Gaining the confidence of well-known companies would help us project a very good image.

Second, we wanted to get support from an established software technology company. There had been much speculation in the press that the big software companies were aggressively targeting the markets of some of the new B2B companies. We wanted to distance ourselves from the new software technology companies that might easily be made obsolete by established players.

Finally, we wanted some of the big suppliers in healthcare to invest in us. By now, everyone knew that one of the biggest uncertainties in the business models of B2B companies was what the established suppliers might do to resist the newcomers. It makes it very difficult to sell stuff when the seller refuses to sell.

The generic identities of the companies on our list were gradually replaced with actual names. Assorted relationships that Neoforma had already established quickly yielded leads on interested corporate investors.

Dell Computer Corporation had a strategic investment fund that was interested in leading the round. With Dell’s reputation for innovative business management at its peak, adding them to our list would certainly achieve our goal of being associated with a household name.

SAP America, the U.S. branch of the huge enterprise software company, seemed to be a perfect choice as a software technology investor.

Their software had a substantial presence in the offices of healthcare suppliers, as well as at large hospital systems. We had been partnering successfully with SAP for several months. While they didn’t have a fund dedicated to the pursuit of strategic investments, they were very interested in pursuing an investment in us.

We hoped to get an investor in each of three supplier categories: medical equipment, medical supplies and medical distribution. Other than pharmaceuticals, which was an area we weren’t interested in pursuing in the near future, these were the three big areas in healthcare.

In our early days, we had found General Electric to be one of the most stubborn medical equipment manufacturers for us to deal with. Their aggressive pursuit of dominance of each of their markets created such a strong outward force that their corporate policies were nearly impenetrable. They did not like the idea of allowing upstart companies to get so much as a foothold in their domain.

Though we had been cautiously probed by some of their largest competitors, GE had shut its doors tightly on us. They made it clear to us that they believed there was nothing we could do that they couldn’t do better on their own.

Then, as we were building up to the IPO, GE called us. They wanted to talk. One of the lead managers in their strategic investment fund had seen Bob speak at an investor conference and reported that Neoforma held far and away the most exciting potential of any company he’d heard about at the show. That got the attention of GE management.

Healthcare was a large part of GE’s business and yielded among the most consistent and lucrative profits. The margin—the amount of money made on each sale—was very high in healthcare equipment. If there were a company out there that might threaten those margins, and if that company were to acquire enough assets, well—that would be very bad for executive bonuses.

So, GE had done some very serious investigation of the increasing numbers of B2B healthcare companies and had come to the conclusion that Neoforma was simultaneously the strongest and least threatening of the bunch. At least that’s what they told us.

We certainly couldn’t argue with their conclusion. We were the strongest and we had always held a participatory, rather than confrontational, position with suppliers. Our main competitor, Medibuy, was openly and foolishly promoting a let’s band together and screw the manufacturers message to potential hospital customers.

We had no doubt that GE considered us the lesser of evils, rather than the greater of opportunities—but, hey, they were GE, and GE was the undisputed U.S. leader in healthcare equipment.

In an initial meeting with us, the GE representatives had come in with a very condescending attitude. When we made it apparent that we didn’t consider them much more important than the other ten thousand medical manufacturers, they were visibly startled. The tone of the conversation changed quickly. After a few meetings, they informed us that they would be happy to extend to us the privilege of consideration for investment. And we told them that we’d be happy to listen to what they had to say.

GE was to healthcare equipment what Johnson & Johnson was to healthcare supplies. And it just so happened that J&J was interested in us too — though for a very different reason. Whereas GE saw us as a threat, J&J saw us as an opportunity. They did not like what the group purchasing organizations had done to their margins in the supplies markets. They wanted to crush the GPOs. They saw Neoforma as a chance to do just that. But that meant, they’d need some control over us. When they expressed their interest in investing, we said okay.

The largest distributor of healthcare supplies was Cardinal. When Bob accepted the top job at Neoforma, he had been certain that Cardinal would be enthusiastic about investing in our strategic round. But when Bob’s former boss at Cardinal decided that Bob had betrayed the company by leaving, that was no longer a possibility. Fortunately, there were several other large distributors with which we were on friendly terms, so we discussed strategic investment possibilities with them. Two of them thought this was a good idea.

Several of our previous venture firms and many new ones wanted to play too. Jeff and I were both receiving calls from venture firms all over the country, espousing their connections and expertise, asking to be considered for participation in the funding round. They were offering to put millions in, no questions asked.

One of the calls was from Jack, our mentor and first attorney. He told me that a partner from one of the first venture firms we had

made a presentation to, two years earlier, had called him to ask “a big favor.”

He wanted Jack to convince Jeff and me to include his firm in the round.

I could tell that Jack was perversely thrilled to deliver this message. I remembered our presentation to this guy very well. He had been among the most dismissive and condescending VCs we had met. And that was saying a lot.

Jack knew our answer, but wanted to hear us say it. He had been so enthusiastic about us at the time and had been very upset that the VCs didn’t see why. He had taken it personally. It was a pleasure for him to deliver our answer personally.

Everything seemed to be lining up nicely. This list of investors was more than we could have hoped for. I was very excited by the knowledge that our team of partners could not possibly be topped by Medibuy, however powerful their keiretsu was.

Keiretsu is a term borrowed from the Japanese. It refers to a conglomerate of businesses linked together by a common financial interest. The term had become associated with KP because of the way they were leveraging the power of companies they’d previously invested in to support their newer investments. We knew they were trying very hard to gain ground on us. KP was not used to settling for second place.

With such a powerful list of investors lining up behind Neoforma, all we had to do was to work out the details. In a few short months, we needed to get them all to agree to a set of financial terms that were favorable to us. The higher our valuation, the lower our dilution would be and the more money our investors could recover after the IPO.

To be continued...

RSS Feed

RSS Feed